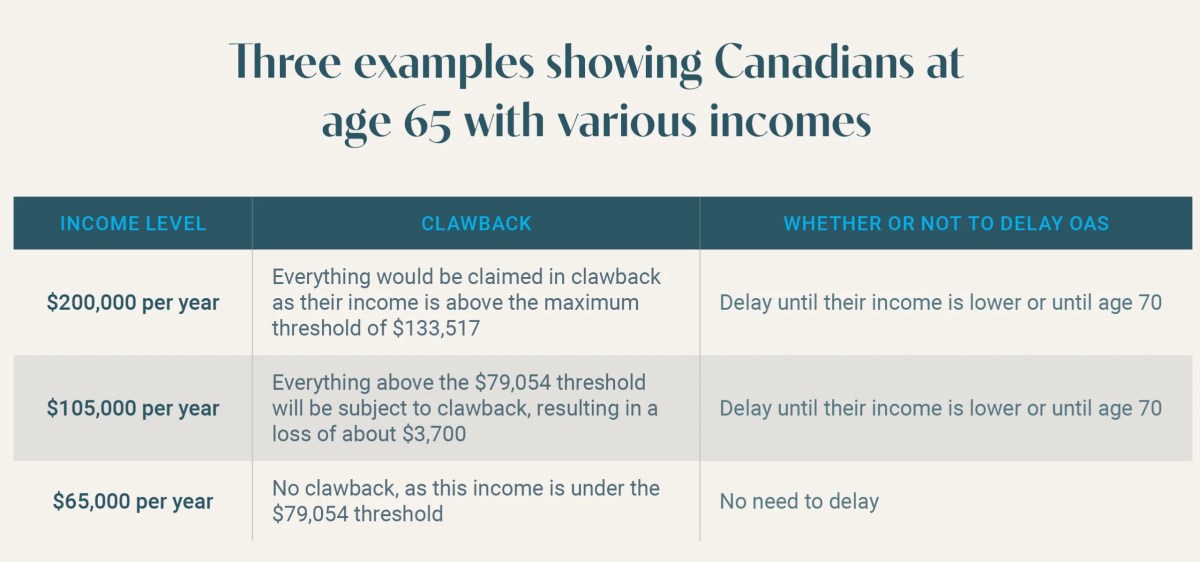

Canada January 2025 OAS Boost: Get ready for a significant increase in Old Age Security (OAS) benefits! Starting January 2025, Canadian seniors will see a boost to their monthly payments, impacting their finances and overall well-being. This increase, driven by inflation and government policy, will offer a much-needed financial cushion for many. Let’s explore the details and what this means for you.

We’ll delve into the projected percentage increase, examine how different income levels will be affected, and analyze the broader economic implications for Canadian seniors. We’ll also compare the OAS increase to adjustments in other pension plans like the CPP and discuss the long-term sustainability of the OAS program. Get ready to understand how this boost will shape the financial landscape for Canadian retirees.

Projected OAS Increase in January 2025

The Old Age Security (OAS) benefit is set to receive an increase in January 2025, impacting the monthly payments received by millions of Canadian seniors. This adjustment is tied to the rate of inflation and is a key element of the government’s commitment to ensuring seniors maintain a reasonable standard of living.

Factors Influencing the OAS Increase

The primary driver behind the projected OAS increase is inflation. The Canadian government uses the Consumer Price Index (CPI) to measure inflation and adjust various social programs, including OAS, to maintain their purchasing power. A higher CPI translates to a larger percentage increase in OAS payments. Government policy plays a crucial role as well; the government decides the formula for calculating the increase and sets the parameters for the annual adjustment.

For example, the government may choose to implement a partial indexation to mitigate budgetary pressures while still providing seniors with some inflation protection. The specific percentage increase for January 2025 will depend on the average CPI calculated over a specific period, usually the previous year.

Projected Percentage Increase and Monthly Payment Increase

While the precise percentage increase for January 2025 isn’t definitively known until closer to the date (as it’s based on the final CPI calculation), let’s assume, for illustrative purposes, a projected increase of 3%. This is a hypothetical example and may not reflect the actual increase. A 3% increase on a current monthly OAS payment of $687.66 (as of October 26, 2023 – this number will change by January 2025), would result in an additional $20.63 per month.

This would bring the new monthly payment to approximately $708.29. It’s crucial to remember that the actual increase will vary based on the final CPI calculation and individual circumstances, such as additional GIS or other government benefits.

Comparison of OAS Payments Before and After the January 2025 Increase (Hypothetical Example)

The following table provides a hypothetical comparison of OAS payments before and after a 3% increase. Remember, these figures are for illustrative purposes only and are based on a projected 3% increase. The actual increase will vary.

| Income Level | Current Monthly Payment (Hypothetical) | Increased Monthly Payment (Hypothetical, 3% increase) | Percentage Increase |

|---|---|---|---|

| Low Income | $687.66 | $708.29 | 3% |

| Middle Income | $687.66 | $708.29 | 3% |

| High Income | $687.66 | $708.29 | 3% |

| Note: These figures are hypothetical examples only and are subject to change. Actual figures will be released by the government closer to the date of the increase. |

Impact on Canadian Seniors: Canada January 2025 Oas Boost

The projected OAS increase in January 2025 will have a significant impact on the economic well-being of Canadian seniors. This additional income, while seemingly modest for some, can represent a substantial boost to the budgets of many older adults, particularly those living on fixed incomes or near the poverty line. The effects will ripple through various aspects of their lives, influencing spending patterns, financial security, and overall quality of life.The increased OAS payments will directly affect seniors’ living standards.

Okay, so you’re looking at the Canada January 2025 OAS boost, right? That’s a pretty big deal for seniors. But did you hear about this crazy story? Apparently, a drone hit a firefighting plane – check out the details here: drone hits firefighting plane. It makes you think about how even small things can have huge consequences, especially when we consider the impact of the upcoming OAS increase on so many people’s lives.

For many, the extra money will translate into a greater ability to meet essential needs such as food, housing, and medication. This could alleviate financial stress and improve their overall health and well-being. For example, a senior struggling to afford prescription drugs might now be able to fill their prescriptions without compromising other essential expenses. This improved access to healthcare can lead to better health outcomes and reduced reliance on emergency services.

Changes in Spending Habits and Financial Security

The additional income from the OAS boost will likely influence how seniors allocate their resources. Some might choose to increase their spending on discretionary items, such as social activities, travel, or hobbies, leading to improved mental and social well-being. Others may prioritize debt reduction, saving for future expenses, or contributing to family support. For instance, a senior who previously delayed necessary home repairs might now be able to afford them, improving their living conditions and safety.

Conversely, a senior might use the extra funds to help their grandchildren with education costs, strengthening family ties and providing intergenerational support. This increased financial flexibility contributes to a sense of security and reduces anxieties surrounding unexpected expenses.

Implications for Senior Poverty Rates and Income Inequality

The OAS increase has the potential to positively impact senior poverty rates and reduce income inequality among older Canadians. By providing a more substantial safety net, the increase could lift some seniors above the poverty line and lessen the gap between the wealthiest and poorest elderly individuals. However, the magnitude of this impact will depend on factors such as the size of the increase, the cost of living, and the distribution of the additional income across different income groups.

For example, a substantial increase might significantly reduce poverty among low-income seniors, while a smaller increase might have a more limited effect. The effectiveness of the OAS increase in addressing income inequality will also depend on other social policies and programs aimed at supporting vulnerable senior populations.

Potential Uses of Extra OAS Funds

The extra OAS funds offer seniors increased flexibility in managing their finances. Below are some potential ways they might utilize this additional income:

- Improved Healthcare Access: Paying for prescription drugs, dental care, or vision care.

- Enhanced Housing Security: Covering rent or mortgage payments, making necessary home repairs, or adapting their homes to accommodate age-related needs.

- Increased Social Participation: Engaging in social activities, travelling, or pursuing hobbies.

- Debt Reduction: Paying down credit card debt or other outstanding loans.

- Emergency Fund: Building or replenishing an emergency fund to cover unexpected expenses.

- Family Support: Assisting family members with financial needs.

- Saving for the Future: Contributing to retirement savings or investing for future expenses.

Government Budgetary Considerations

The January 2025 OAS increase represents a significant budgetary commitment for the Canadian government. Understanding how this increase is funded and its impact on overall government spending is crucial for assessing its long-term fiscal implications. This section examines the budgetary allocation, funding sources, comparative costs, and the projected long-term fiscal sustainability of the OAS program following this boost.The government’s budgetary allocation for the OAS increase in the 2025 budget would likely be detailed within the main budget document released by the federal government.

While the precise figure isn’t available at this pre-budget stage, we can project based on previous increases and the anticipated number of seniors receiving OAS. The increase will necessitate a substantial increase in government spending, requiring careful consideration of other budgetary priorities.

Funding Sources for the Increased OAS Payments

The increased OAS payments will be funded through a combination of sources. Tax revenues, including income tax, GST/HST, and corporate taxes, form the primary source. The government might also consider adjustments to other programs or explore alternative revenue streams, depending on the overall fiscal situation and priorities. For example, a scenario similar to previous budget adjustments might involve minor cuts to less impactful programs, a slight increase in certain taxes, or a strategic reallocation of funds from other areas.

It’s important to remember that these are potential scenarios and the actual funding sources will be clearly Artikeld in the official budget.

Cost of the OAS Increase Compared to Other Government Spending Programs

Comparing the cost of the OAS increase to other government spending programs requires a detailed analysis of the budget. This would involve examining the total expenditure on areas such as healthcare, education, defense, and social welfare, then placing the OAS increase within this context. For example, one could compare the cost to the annual budget of the Canadian Armed Forces or the amount spent on healthcare subsidies.

The relative size of the OAS increase compared to other major programs helps to contextualize its budgetary impact. A visual representation, such as a bar chart comparing spending across different departments, would effectively illustrate this comparison.

Long-Term Fiscal Sustainability of the OAS Program

The long-term fiscal sustainability of the OAS program, considering this increase, depends on several factors. These include population aging, economic growth, and future government policy decisions. A growing elderly population will inevitably increase the cost of the OAS program over time. Sustaining the program will require ongoing economic growth to support tax revenue and careful management of government spending.

The government might need to implement measures to mitigate future cost pressures, such as adjusting eligibility criteria or exploring alternative funding models. The long-term sustainability assessment usually includes demographic projections and economic forecasts, along with sensitivity analysis to account for uncertainties. For example, a projection might consider different scenarios for economic growth and population aging to estimate the potential impact on OAS expenditures over the next 20-30 years.

This type of analysis will be essential in formulating long-term fiscal strategies.

Comparison with Other Pension Programs

The January 2025 OAS increase needs to be viewed within the broader context of Canada’s retirement income system. Understanding how it interacts with other key programs, like the Canada Pension Plan (CPP), is crucial for assessing its overall impact on seniors’ financial well-being. This section compares the OAS adjustment to changes in other pension plans and examines the combined effect on retirement income.

Okay, so you’re wondering about the Canada January 2025 OAS boost? That’s a big deal for seniors! But let’s say a wildfire breaks out – that’s where things get serious, and you might see a super scooper plane in action fighting the flames. Knowing about both the OAS increase and the potential for these firefighting aircraft helps you understand the different ways Canada prepares for the future.

OAS Increase Compared to CPP Adjustments, Canada january 2025 oas boost

The yearly increase to OAS is determined by the rate of inflation, while CPP adjustments are more complex. CPP benefits are indexed annually to inflation, but the maximum contribution and benefit amounts are also reviewed and adjusted periodically based on wage growth and demographic factors. Therefore, while both programs aim to protect retirees from inflation, the mechanisms and resulting increases may differ from year to year.

For example, in a year with high inflation, the OAS increase might be significant, but the CPP increase might be more modest if wage growth lags behind. This difference can impact the overall retirement income for seniors who rely heavily on either program.

Adequacy of OAS Benefits Relative to the Cost of Living

The adequacy of OAS benefits for Canadian seniors is a continuous subject of debate. While OAS provides a crucial base level of income, its adequacy varies significantly depending on individual circumstances, such as location (cost of living varies across provinces), health status, and other sources of income. For many seniors, particularly those living alone or in high-cost areas, OAS alone may not cover essential expenses, leading to financial strain.

Supplementing OAS with other income sources, such as CPP, private pensions, or savings, is frequently necessary to maintain a reasonable standard of living.

Combined Impact of OAS and Other Pension Plans

The combined effect of OAS and CPP, along with other potential sources of retirement income like private pensions and savings, is what truly determines a senior’s financial security. The OAS acts as a foundational safety net, providing a guaranteed minimum income. The CPP, on the other hand, provides a larger, contributory benefit based on individual earnings during working years.

The interplay between these two programs, along with other sources, significantly influences the overall retirement income of seniors. A senior with a high CPP contribution history and additional private pension income will have a much more comfortable retirement than a senior who solely relies on OAS and a small CPP benefit. This highlights the importance of a multi-faceted approach to retirement planning.

Summary of Key Pension Programs

| Program | Key Features | Approximate Benefit Amount (2025 – illustrative example) |

|---|---|---|

| Old Age Security (OAS) | Universal, means-tested, age 65+, indexed to inflation | $700 – $1000 per month (depending on income) |

| Canada Pension Plan (CPP) | Contributory, benefit based on earnings history, indexed to inflation | Variable, depending on contribution history; average could be $1000 – $2000 per month |

| Guaranteed Income Supplement (GIS) | Means-tested supplement to OAS for low-income seniors | Variable, depending on income and marital status; can significantly boost OAS for eligible seniors |

Note

Benefit amounts are illustrative examples only and may vary based on individual circumstances and future adjustments. Consult official government sources for the most up-to-date information.

Future Projections for OAS

Predicting the future of the Old Age Security (OAS) program requires considering several interconnected factors. While the January 2025 increase provides a snapshot of current adjustments, understanding long-term trends is crucial for both seniors planning for retirement and policymakers managing the program’s fiscal sustainability. This section explores potential future OAS adjustments, considering inflation, demographic shifts, and potential policy changes.

Projected OAS Adjustments Beyond 2025

Future OAS increases will largely depend on the rate of inflation. The program is indexed to inflation, typically using the Consumer Price Index (CPI). Therefore, projections hinge on forecasts for CPI growth. For example, if economists predict an average annual inflation rate of 2% over the next decade, we can expect roughly a 2% annual increase in OAS benefits, although this is a simplification and doesn’t account for potential changes in the indexing methodology.

However, periods of higher or lower inflation will directly influence the yearly adjustments. A period of high inflation, such as experienced in recent years, will result in larger annual increases, while lower inflation would lead to smaller increases. Unforeseen economic shocks could also significantly alter these projections.

Okay, so you’re looking at the Canada January 2025 OAS boost? That’s great news for seniors! But think about this: how will those extra funds help if a wildfire breaks out, requiring the rapid deployment of resources like a super scooper plane for water bombing? It highlights how even with increased income, unexpected events can still impact our lives, reminding us to be prepared for anything.

Back to that OAS boost though – make sure you understand how to access those funds!

Potential Policy Changes Affecting OAS Benefit Levels

Government policy plays a significant role in shaping future OAS benefits. Potential changes include adjustments to the eligibility age, changes in the benefit calculation formula, or the introduction of means-testing (where benefits are reduced for higher-income seniors). For example, increasing the eligibility age from 65 to 67, a measure considered in some countries, would delay the receipt of benefits for a significant portion of the population and thus reduce the overall financial burden on the program.

Similarly, introducing means-testing could save considerable public funds, but it would likely face considerable political and social resistance.

Long-Term Sustainability of the OAS Program

The aging population poses a significant challenge to the long-term sustainability of OAS. As the proportion of seniors in the population increases, the number of OAS recipients will rise, placing greater pressure on government finances. This is a challenge shared by many developed nations with aging populations. To ensure the long-term viability of the program, the government may need to implement a combination of strategies including the aforementioned policy changes, exploring increased contributions, or adjusting benefit levels in line with economic realities.

The sustainability of OAS is directly linked to the overall health of the Canadian economy and its ability to fund social programs.

Impact of Different Economic Scenarios on Future OAS Adjustments

Economic downturns, such as recessions, can significantly impact OAS adjustments. During a recession, government revenues may decrease, limiting the government’s ability to increase benefits or maintain existing levels. Conversely, periods of strong economic growth can provide greater fiscal flexibility, potentially allowing for more generous increases in OAS benefits. For instance, a prolonged recession could lead to a temporary freeze or even a reduction in the annual increase, whereas a period of sustained growth might allow for increases exceeding the rate of inflation.

The Canadian government would need to balance its budget priorities while responding to the needs of seniors in both scenarios.

Outcome Summary

The Canada January 2025 OAS boost represents a significant development for Canadian seniors. Understanding the projected increase, its impact on various income levels, and its comparison to other pension programs is crucial for financial planning. While the increase offers welcome relief, it’s essential to consider the long-term sustainability of the OAS and its role in ensuring a secure retirement for future generations.

Stay informed and plan ahead to maximize the benefits of this important adjustment.

Clarifying Questions

Will the OAS increase affect everyone equally?

No, the percentage increase will be applied to the existing OAS payment, meaning higher-income seniors will receive a larger dollar amount increase than lower-income seniors.

How is the OAS increase funded?

The funding comes from general government revenue, meaning various taxes and government programs contribute to the OAS budget.

When will I receive the increased OAS payment?

The increased payments should begin with your January 2025 OAS payment.

What if I’m already receiving the Guaranteed Income Supplement (GIS)?

The GIS will also increase proportionally with the OAS increase.